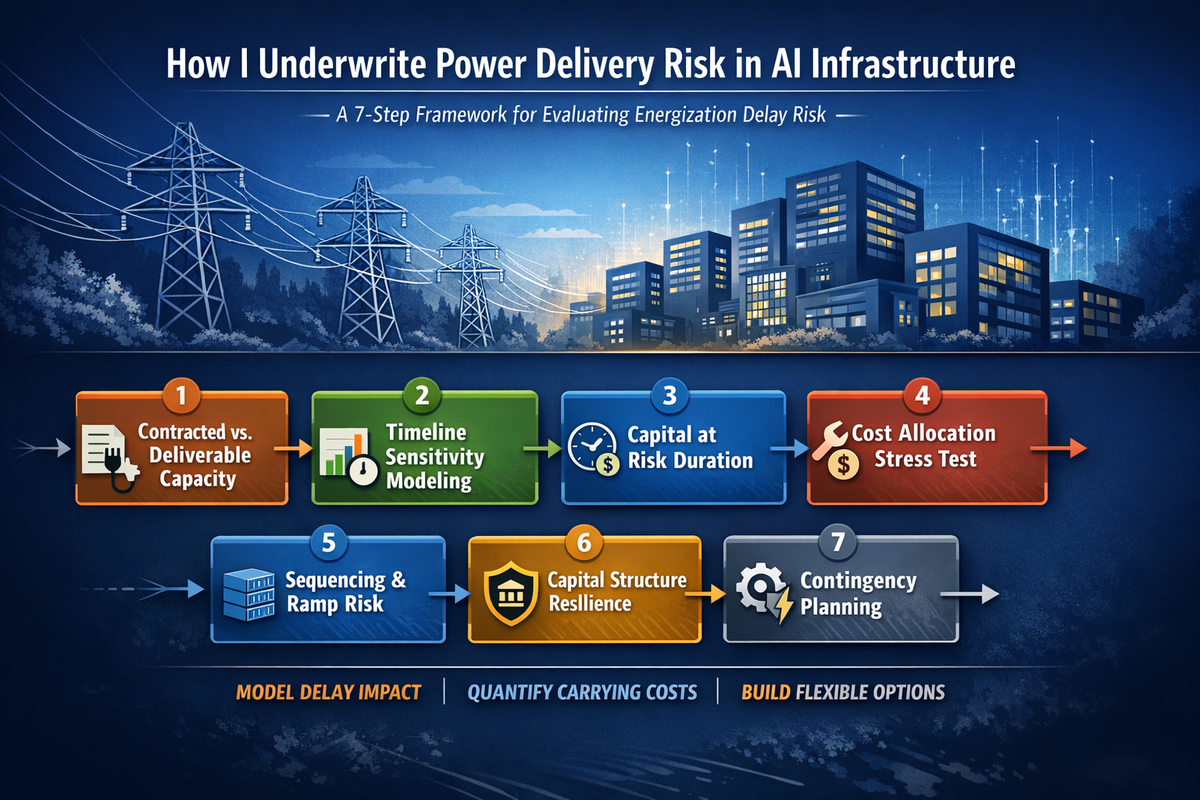

How I Underwrite Power Delivery Risk in AI Infrastructure

February 18, 2026

AI demand is accelerating.

Capital is available.

Land is trading.

But in every AI data center investment I evaluate, one variable dominates the return profile more than most people admit:

Power delivery timing.

Not demand.

Not lease rates.

Not exit multiple.

Timing.

Below is the structured framework I use when underwriting power risk in AI builds.

This is not theoretical.

It is how I pressure-test projects before capital is committed.

Step 1: Separate Power Into Two Categories

The first mistake I see is treating “secured power” as a single concept.

It is not.

There is:

- Contracted capacity

- Deliverable, energized capacity

Those are very different risk profiles.

A signed interconnection agreement does not equal electrons at the meter. A queue position is not the same as energized infrastructure.

Underwriting starts by isolating where the project truly sits along that spectrum.

If the model assumes energization at Month 36, I ask:

What percentage probability does that date actually have?

If that question makes people uncomfortable, the risk is real.

Step 2: Build a Timeline Sensitivity Model

Most models treat energization as a fixed date.

I treat it as a probability distribution.

Instead of one COD assumption, I model:

- Base case energization

- +6 month slip

- +12 month slip

- +18 month slip

Then I evaluate what happens to:

- IRR

- Equity multiple

- Debt service coverage

- Cash burn

In AI builds, a 12–18 month delay often compresses equity returns far more than moderate lease rate pressure.

Why?

Because AI capital is front-loaded.

Land, shell, electrical gear, cooling infrastructure, capital is deployed early.

Revenue begins only after commissioning.

If commissioning moves, the carrying cost compounds.

Delay is not linear.

It is multiplicative.

Step 3: Quantify Capital at Risk Duration

This is where many investors underestimate exposure.

I calculate:

Total capital deployed before revenue begins

×

Weighted average cost of capital

×

Expected delay scenarios

This creates a “capital at risk duration” number.

For example:

If $600M is deployed before stable energization and a 12-month delay occurs, the incremental cost of capital alone can materially shift project returns before accounting for lost EBITDA timing.

Most models focus on total project cost.

I focus on time-exposed capital.

Time is a financial variable.

Step 4: Stress Test Cost Allocation Risk

Transmission upgrades are not always fixed.

Study revisions can change:

- Scope

- Responsibility

- Cost allocation

I ask three questions:

- Are upgrade costs capped contractually?

- Who absorbs overruns if scope expands?

- What historical variability has the utility shown in similar load requests?

If upgrade exposure is open-ended, that risk deserves its own contingency reserve in the model.

Not a footnote.

A line item.

Step 5: Evaluate Sequencing Risk

AI deployments are rarely incremental.

They tend to be lumpy.

If a hyperscaler intends to deploy 40 MW in one block, partial energization may not generate partial revenue.

This creates step-function revenue risk.

So I model:

- Revenue assuming full energization

- Revenue assuming staged energization

- Revenue assuming anchor tenant delay

If revenue is dependent on synchronized energization, timeline sensitivity must widen.

Step 6: Overlay Capital Structure Resilience

This is where finance discipline matters most.

I pressure-test:

- Interest reserve sufficiency

- Construction debt maturity timing

- Covenant flexibility

- Equity bridge capacity

If energization slips 12–18 months, can the capital stack absorb it?

Or does refinancing risk emerge before revenue stabilizes?

The difference between a well-structured AI build and a stressed one often lies here, not in demand assumptions.

Step 7: Assess Contingency Optionality

Finally, I look at flexibility.

Can temporary generation bridge a portion of load?

Can deployment be phased geographically?

Is there diversification across multiple substations?

Optionality reduces binary exposure.

Projects without contingency paths carry asymmetric downside.

What This Framework Changes

When you apply this structure, something interesting happens.

The conversation shifts from:

“How large is the opportunity?”

To:

“How durable are the returns under timeline stress?”

It becomes less about megawatts announced

And more about megawatts monetized.

That shift is where capital discipline lives.

Why This Matters Now

AI infrastructure is entering a scale phase.

Scale amplifies small modeling errors.

If you underwrite 10 MW incorrectly, the impact is manageable.

If you underwrite 200 MW incorrectly, the consequences compound quickly.

The grid is adapting. Utilities are working hard. Operators are getting smarter.

But physics and sequencing still govern outcomes.

Markets eventually reward the operators who price that reality honestly.

AI demand is real.

The opportunity is real.

But power delivery timing will determine who converts ambition into cash flow.

And underwriting timing properly is what separates enthusiasm from discipline.

"The content is based on public information and personal analysis. This is not financial or investment advice."